Traditionally, Latin America has been perceived as an attractive destination for investment, supported by a growing middle-class population, low labour costs, and an abundance of natural resources. Despite these opportunities for growth, the region has been plagued with economic sluggishness and fears of populist nationalism resurging.

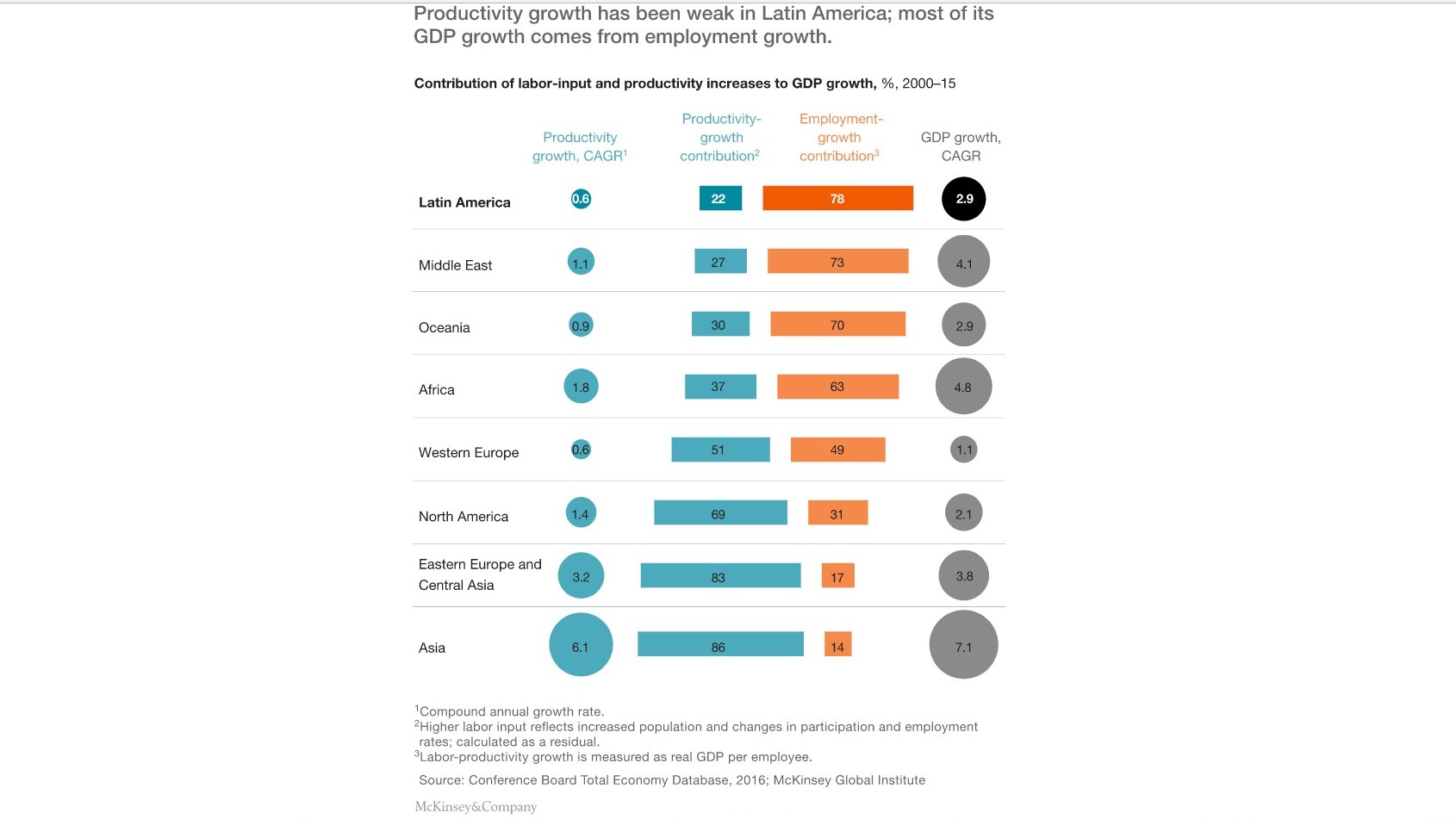

Between 2000 and 2015, Latin American economies have achieved an average annual GDP growth of three percent, constituting a relatively underwhelming performance compared to other developing regions. This can be partly attributed to the region’s relatively weak growth in productivity, which has only risen by close to one percent in the same period. [1] The strong anti-establishment mood accumulated over a plethora of corruption scandals in recent years- most notably the impeachment of former Brazilian President Dilma Rousseff in 2016- continues to grow in the region. Yet, it is precisely for these reasons that 2018 will be the year where Latin America comes under great scrutiny for emerging-market watchers, where all but one of its top five economies will be electing a new president by the end of the year. [2]

The obstacles posed by the slow growth in productivity across Latin American economies are immense. While the region’s working and youth populations are set to be the prime drivers of economic growth through consumption, the decline in fertility rate is likely to be a more disruptive force. As the present commodity supercycle that has fuelled growth particularly in the Andes region comes to an end, Latin America can no longer afford to rely on the next commodity supercycle for its next phase of economic growth.

Unless Latin America attempts to boost the income levels of its rapidly expanding middle-class and engage in high-value-adding economic activities, it is difficult to envision the region diversifying its economic base to raise its competitiveness and drive sustainable economic growth. The Bolsa Familiar programme in Brazil may have drastically reduced the country’s poverty rate by nearly fifty percent in its first decade of implementation, but this has yet to pay off in terms of propelling this segment of the population into real prosperity. [3] Latin American investment of slightly less than one percent of GDP in research and development (R&D) activities also significantly pales in comparison with the OECD region (about three percent) and China (approximately two percent) respectively. Externally, the gloomy outlook of rising American protectionism looks to threaten Latin American trade, given that the USA is the largest importer at forty-five percent of Latin American exports. [1]

In the immediate term, the upcoming elections are bound to narrow the timeframe for enacting urgent reforms as politicians focus on their respective campaigns. Indubitably, the uncertainty is building up around the possibility that parliaments will become more divided following the polls. On the other hand, opportunities could arise if new political leaders manage to secure strong mandates and implement the necessary macroeconomic reforms. In Argentina, President Mauricio Macri successfully signed a landmark fiscal agreement with regional governors last November. Despite lacking a parliamentary majority, his political capital coupled with a politically fragmented opposition contributed to his success in legislating crucial reforms to correct Argentina’s severe fiscal deficit. [4] In contrast, strong opposition to outgoing Chilean President Michelle Bachelet’s reform programme has contributed to the decline in business confidence and private investment in recent years. Newly-elected President Sebastian Pinera has planned investments of 20 billion USD in the next eight years into public-private infrastructure projects to inject certainty into the Chilean business climate. [5] While Mexico is on-track for GDP growth of over two percent, uncertainty regarding North American Free Trade Agreement (NAFTA) negotiations and concerns over the presidency of populist outsider Andres Manuel Lopez Obrador weigh heavily on market sentiment. [4]

What then lies ahead for Latin American in 2018 amidst its seemingly dismal economic productivity and political future? Firstly, the two-round election format provides some form of protection from an extreme election outcome. In the run-off round, which was the case for Chile and is likely to be similar for Costa Rica, Colombia and Brazil, voters tend to go for the more centrist candidate. [6] Secondly, there is room for greater collaboration public and private sectors to join forces to raise productivity and boost consumer expenditure. Governments in Latin America can tap on the connections across the region to expand intraregional trade, promote regional business partnerships and create digital networks. Meanwhile, the private sector can explore riding on the likes of Chilean retailer Falabella’s recently announced expansion into Mexico and Colombian enterprise Empresa Publicas de Medellin’s role in funding major infrastructure projects in Medellin for its revitalization. [3]

Bibliography

[1] Andres Cadena, Jaana Remes, Nicolas Grosman, and Andre de Oliveira, (APR 2017), How to counter three threats to growth in Latin America

[2] The Economist, (2017), Turning tides: A guide to Latin America’s busy 2018 election year

http://pages.eiu.com/rs/753-RIQ-438/images/LATAM_elections_2018_FINAL.pdf

[3] Andres Cadena, Patricia Ellen, Jaime Morales, and Jaana Remes, (JUN 2016), Can Latin America reignite growth by connecting with consumers?

[4] Angela Bouzanis, (DEC 2017), Economic Snapshot for Latin America

https://www.focus-economics.com/regions/latin-america

[5] Pablo Riveroll, (JAN 2018), Latin America focus: can politics boost the growth outlook in 2018?

[6] The Economist, (NOV 2017), Latin America’s voteathon

Edited by Luke Doyle, (BSc. Economics and Economic History)